Trading platform

Trading platform

Monitoring

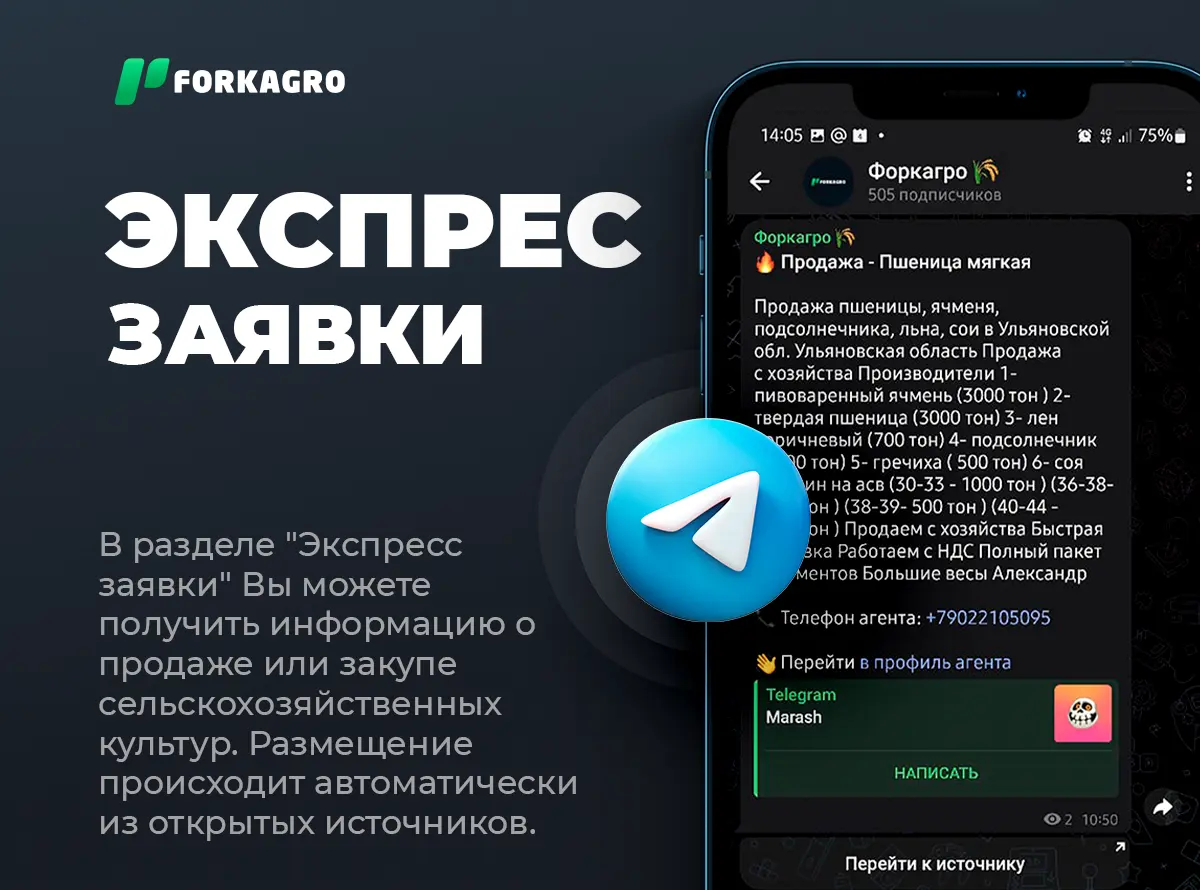

Monitoring  Express applications

Express applications

Fork Work

Fork Work

Service

Service  News

News  Directory

Directory

The decision of the Bank of Russia's Board of Directors, made on March 22, 2024, is to maintain the key rate at 16.00% per annum. Currently, inflationary pressures are gradually easing but remain quite high. Domestic demand continues to significantly outpace the expansion capabilities of goods and services production. Meanwhile, the labor market is becoming even tighter. It is too early to draw conclusions about the speed of disinflation processes. However, the monetary policy carried out by the Bank of Russia will contribute to the disinflation process in the economy.

The return of inflation to the target level in 2024 and its further stabilization around 4% imply a prolonged period of maintaining tight monetary conditions in the economy. According to the Bank of Russia's forecast, with the current monetary policy in place, annual inflation will decrease to 4.0–4.5% in 2024 and will remain around 4% thereafter.

The trend of price growth, considering seasonality, remained at the January level in February, and according to preliminary data, started to decline in March. Different tendencies were observed in the consumer basket: a slowdown in the price increase of goods was accompanied by acceleration in services. The annual inflation rate remains at the February level, estimated at 7.7% as of March 18.

Despite the tightening of monetary conditions, high domestic demand contributes to maintaining elevated inflationary pressure. Most stable indicators of current price growth, presented by the Bank of Russia, range between 6-7% on an annual basis. The core inflation rate, considering seasonality, increased to 7.7% annually in February (up from 6.8% in January), primarily due to the rise in the cost of foreign tourism services. Excluding this factor, core inflation remained almost unchanged.

Inflation expectations of the population and price expectations of enterprises continue to decrease. However, they still remain at a relatively high level, which contributes to inertia in the current elevated price growth.

Operational indicators indicate that the Russian economy continues to grow rapidly in the first quarter of 2024. Consumer activity remains high due to significant income growth and confident consumer sentiments. Business surveys data indicate the preservation of a high investment demand. The deviation of the Russian economy from the trajectory of balanced growth remains significant.

The main obstacle to the expansion of goods and services production is the shortage of labor resources. Simultaneously, the labor market is becoming even tighter with the unemployment rate hitting a historical low.

Monetary policy conditions have become tighter following the increase in the key rate in the second half of 2023. Nominal and real interest rates are rising across different segments of the financial market. There is a stable inflow of personal funds into time deposits. The growth rate of corporate and mortgage lending has been declining since the beginning of the year. However, there is an acceleration in unsecured consumer lending in the retail segment. Rising incomes allow the population to increase savings and consumption simultaneously. The effects of previous key rate hikes will continue to influence the dynamics of lending in the upcoming months. Additional tightening of banking lending conditions will occur due to the implementation of several macroprudential measures and the rollback of most regulatory easings for banks.

On a medium-term horizon, inflation risks are still tilted towards an increase. The main pro-inflation risks are related to changes in foreign trade conditions (including geopolitical factors), maintaining high inflation expectations, overachievement of expected indicators of balanced growth in the Russian economy, and the trajectory of budget policy normalization. Disinflationary risks are mostly tied to a faster decline in domestic demand than expected in the base scenario.

A summary of the discussion on the key rate will be published by the Bank of Russia on April 1, 2024.

The next meeting of the Bank of Russia's Board of Directors to discuss the key rate level is scheduled for April 26, 2024. A press release on the decision of the Bank of Russia's Board of Directors and the medium-term forecast will be published at 13:30 Moscow time.