Trading platform

Trading platform

Monitoring

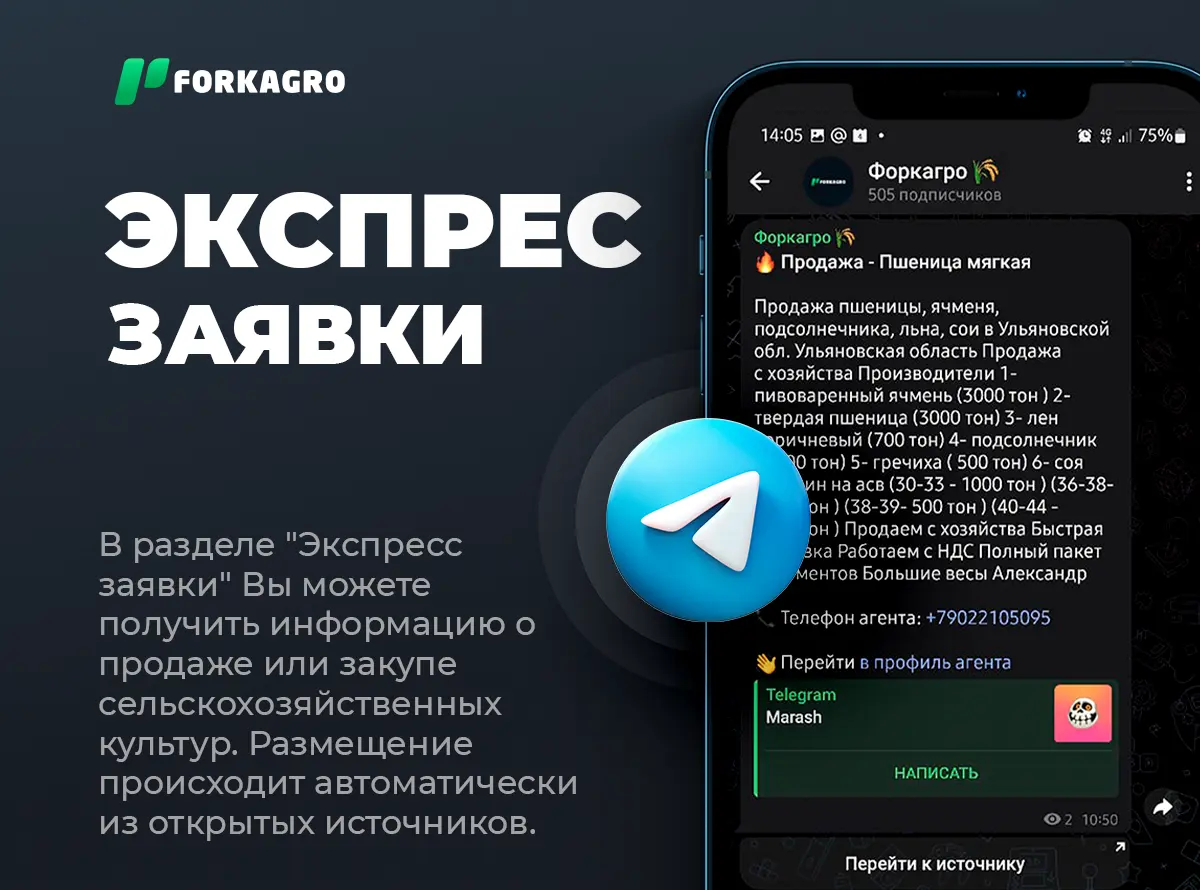

Monitoring  Express applications

Express applications

Fork Work

Fork Work

Service

Service  News

News  Directory

Directory

Increased activity of foreign importers, dynamic purchases into the state fund and active exports in the first ten days of January indicate a possible increase in wheat prices. There is a gap in the market between actual prices at ports and estimated levels, and it is expected that ruble prices will soon begin to close it. As for the sunflower market, stability is predicted: a sharp drop in prices after active growth is not expected. Soybean prices are at a comfortable level despite a record harvest.

Regarding wheat on the world market, factors leading to higher prices include continued high rates of wheat purchases by Egypt. At the latest tender of the GASC company (Egyptian state food procurement agency), contracts were signed for 420 thousand tons, of which 360 thousand tons were wheat of Russian origin at a price of 265 US dollars per ton FOB. 240 thousand tons of wheat were purchased from Jordan, presumably from Russia, with delivery in March-April 2024.

Factors driving down prices include relatively weak exports from the European Union and increasing imports into selected European countries, leading to higher European wheat stocks towards the end of the 2023/24 season.

On the Russian market, factors leading to rising wheat prices include dynamic purchases of grain into the intervention fund: more than 300 thousand tons were purchased, with special attention paid to 3rd and 4th grade wheat. High rates of wheat exports also have an impact on rising prices: since the beginning of January, shipments have exceeded 1 million tons, mainly through Black Sea ports, although offshore transshipment is not operating optimally.

Factors leading to lower prices include the strengthening of the ruble due to an increase in the key rate and currency sales by the Central Bank.

In general, the gap between actual and estimated prices in the ports of the Azov-Black Sea basin is growing as the physical market grows. Wheat prices have already reached $245 per ton, which, even with a strengthened ruble exchange rate, indicates a level of 15,000 rubles per ton excluding VAT (srt-port). Taking into account prices at tenders, including the Egyptian GASC, this figure may be even higher. It is most likely that we will see a gradual increase in quotations from exporters, although this will not happen quickly, and it is unlikely that the potential price will be achieved.

With regard to barley on the world market, no significant factors influencing the rise or fall of prices have been identified. In the Russian market, factors leading to higher barley prices include increased shipping activity: 94 thousand tons have been shipped, and almost 200 thousand tons are being prepared for loading. Factors influencing the decline in prices also include the strengthening of the ruble exchange rate due to an increase in the key rate and currency sales by the Central Bank.

The current ratio of export prices for barley is similar to the wheat market - the gap between actual and calculated levels is 1000-1500 rubles per ton. Potential growth is possible in the next few weeks, but it will also be limited. However, the pick-up in exports seen since late December could support the market.

For corn on the global market, factors driving up prices include lower crop forecasts in Brazil due to unfavorable weather conditions in the first half of December. The subsequent improvement in ground moisture is only partially supporting prices. Factors influencing the decline in prices include confirmation of a record corn harvest in China - 289 million tons (December USDA estimate - 277 million tons).

In the Russian market, factors leading to higher corn prices include active export shipments: more than 170 thousand tons have been shipped since the beginning of January, and the volume of deliveries in the next 7-10 days is 275 thousand tons.